Minister Rob Beenders and Belgian banks step up the fight against online fraud with action plan

8 July 2026 - 9 min Reading time

Over recent months, at the request of Minister for Consumer Protection Rob Beenders, Febelfin has developed a banking sector action plan aimed at reducing online fraud, lowering the number of victims and limiting financial losses. “With this action plan, we are jointly taking important steps to further protect Belgian consumers against online fraud,” declare Rob Beenders and Febelfin.

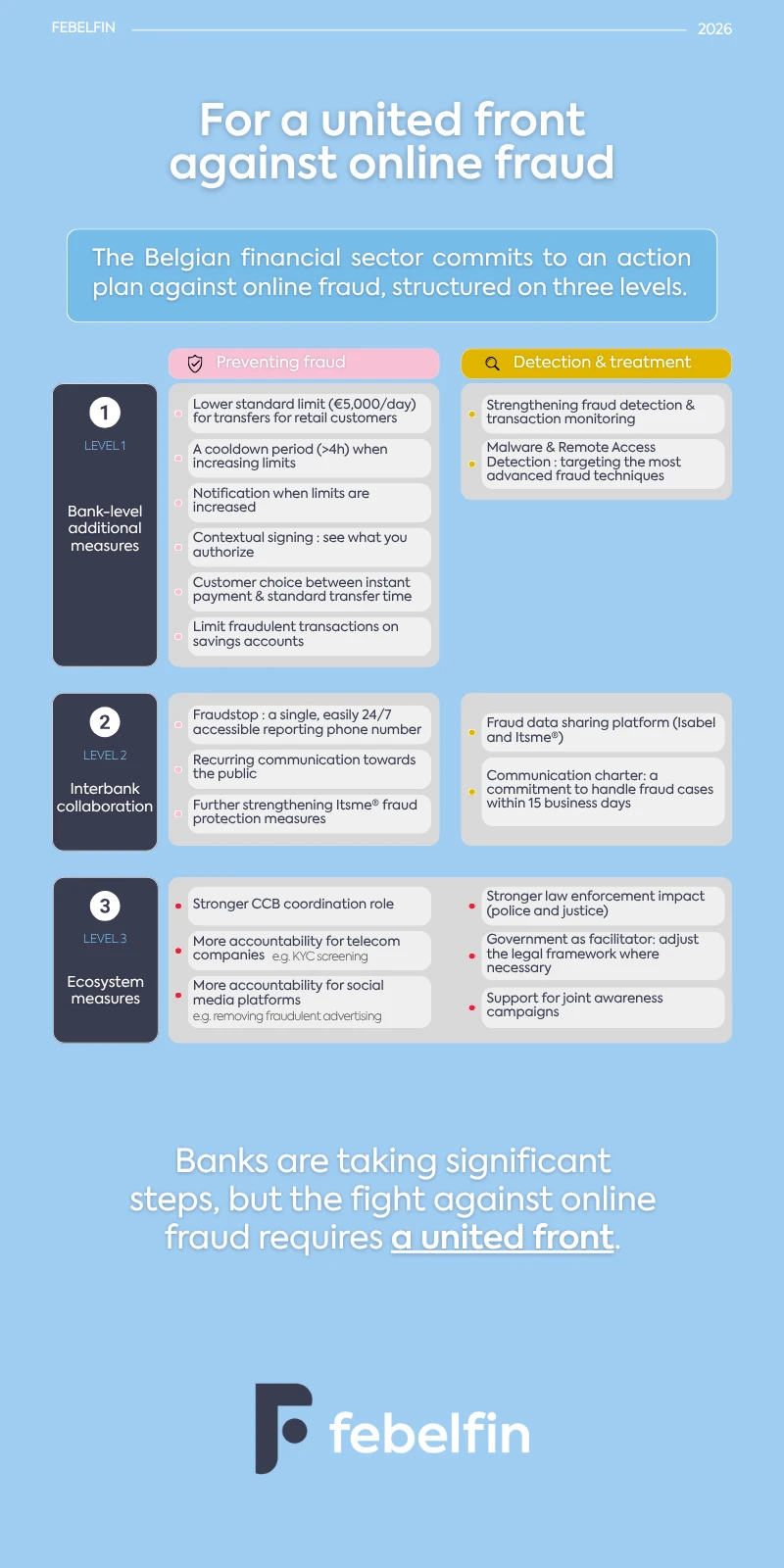

This plan commits the banking sector to additional efforts at three levels: (1) further strengthening individual protection measures by each bank, (2) enhanced cooperation between banks, including the creation of a data-sharing platform and individual victim support, and (3) a comprehensive approach, coordinated by the government, in which all stakeholders assume their responsibilities.

Increased investment in fraud prevention

Online fraud has become a structural and rapidly evolving societal problem. Criminal networks increasingly rely on sophisticated techniques, artificial intelligence and manipulation to deceive victims. Fraud often originates on social media platforms, communication services and other digital channels where fraudsters approach and manipulate consumers. Banks generally only become involved at a later stage of the fraud chain.

For many years, the banking sector has invested heavily in fraud prevention, transaction monitoring and the blocking of suspicious transactions, ... Every day, hundreds of employees across the banking sector are actively engaged in combating online fraud. The sector continues to invest in new security measures that are tailored to fraudsters’ ever-changing methods. In recent months, Minister Rob Beenders has asked banks to go beyond the significant efforts they are already making and take additional action against fraud. The banks are now stepping up the fight together through a new action plan. They commit to implementing further measures, deepening cooperation and calling for the active involvement of the wider ecosystem.

An action plan on three levels

To further strengthen the fight against online fraud, Febelfin has presented to the Minister an action plan built on three pillars, with the objective of preventing fraud even more effectively.

1. Further strengthening prevention and detection measures by individual banks

Each bank commits to introducing additional operational and technical measures to prevent, detect and tackle fraud more rapidly. Today, all banks already apply a selection of such measures to protect their customers. What is new is that the sector is now formulating concrete recommendations to ensure that the full set of measures is implemented within a specified timeframe.

These measures include:

- Action 1: a lower default transfer limit of a maximum of €5,000 per day for private customers. Customers can adjust this limit themselves, either lowering or increasing it;

- Action 2: notifications to customers when transfer limits are increased;

- Action 3: a minimum waiting period of four hours following any transfer limit increase;

- Action 4: Additional measures to further restrict fraudulent transfers from savings accounts to current accounts;

- Action 5: Customer choice between instant payments and standard bank transfers;

- Action 6: Further strengthening fraud detection and transaction monitoring to identify suspicious transactions.

- Action 7: Enhanced authentication procedures clearly displaying what customers are signing or approving.

- Action 8: Improved detection of malware and tools used by fraudsters to gain remote access to customers’ devices.

- Action 9: Identification and, where useful, recommendation of new techniques and developments observed in the market (best practices).

The slow banking measures are specifically designed to disrupt fraud scenarios and provide customers with additional moments for reflection by introducing extra checks and slowing down processes when customers are being pressured by criminals. Their purpose is to help prevent fraud before money is lost, while maintaining the ease of use of digital banking services.

2. Greater cooperation between banks and individual customer support

As fraud often involves multiple banks and accounts, cooperation and information-sharing between financial institutions are essential.

The action plan includes the following measures to prevent online fraud through enhanced cooperation:

- Action 10: Launch of Fraudstop in June, a central telephone number enabling consumers to quickly contact their bank if they suspect online fraud;

- Action 11: Awareness-raising campaigns: Continued investment will be made in campaigns to inform citizens. A key message will be never to share personal banking details. A bank employee will never ask for them;

- Action 12: Itsme® will add additional security layers through innovations in its mobile application. This should reduce the risk of account takeover and prevent fraudsters from confirming logins or payments on behalf of victims.

To detect and combat online fraud:

- Action 13: Fraud data sharing platform: Banks will share fraud signals more quickly and in a more structured manner, allowing suspicious patterns to be identified and stopped sooner. Banks have been advocating this for some time. To make this possible, a supportive legal framework is required. In the future, it should also become possible to exchange information with the telecommunications sector, the police and the judiciary.

- Action 14: Establishment of a communications charter committing the banking sector to handling fraud cases within 15 banking business days and communicating in a consistent manner.

3. A fully-fledged ecosystem approach

Online fraud is now a form of organised crime that extends across the entire fraud chain. Additional banking security measures can mitigate the consequences of fraud, but they will not address its root causes as long as other public and private stakeholders do not contribute proportionately to tackling fraud at its source and ensuring the effective prosecution of criminals.

- Action 15: A joint and integrated approach involving all stakeholders is necessary to sustainably reduce online fraud and prevent Belgium from becoming an attractive target for fraudsters.

Fraud must be tackled at its source by, among others, telecommunications operators, social media platforms and digital service providers. At the same time, further strengthening police and judiciary is essential to detect and prosecute organised fraud more effectively. Febelfin endorses the national action plan for a cross-sector approach to online fraud.

Within the government, agreements have already been reached to work together with all relevant partners on an integrated national anti-fraud strategy. As part of this effort, the government will take on a facilitating role by removing legal obstacles to fraud prevention and enabling greater cooperation. Rob Beenders, Minister for Consumer Protection, and Bernard Quintin, Minister responsible for Home Affairs, are currently leading the development of a national anti-online fraud plan, to which Febelfin will actively contribute.

Conclusion: working together towards a sustainable reduction in online fraud

With this action plan, the banking sector is strengthening its commitment to protecting customers, providing better support to victims and intensifying the fight against online fraud in a coherent and transparent manner. Several measures are already being implemented by a number of banks. Each bank has drawn up its own implementation timetable. The Minister and Febelfin have agreed to remain in permanent consultation to monitor the progress of the plan. This banking sector action plan represents an important step forward in the fight against phishing and online fraud.

Karel Baert, CEO of Febelfin: “Banks are now making additional commitments and continuing to invest in the protection of their customers. However, if we want to structurally reduce online fraud, we must combat fraud at its source, effectively prosecute criminals and hold all stakeholders accountable. Only then can we prevent fraudsters from creating new victims. Because every victim is one too many.”

Rob Beenders, Minister for Consumer Protection: “Online fraud is constantly evolving. That is why it is important that the banking sector now has an action plan to tackle phishing. This is a starting point. We will remain in continuous dialogue and identify new forms of phishing as they emerge, enabling us to respond quickly. If we do not want Belgium to remain an attractive target, everyone must play their part: telecommunications operators, social media and technology companies, as well as the police and judiciary.”

David Clarinval, Deputy Prime Minister and Minister of the Economy: “Phishing is a complex challenge that requires an integrated approach. Through this action plan, the banking sector is making a strong commitment to better protect our citizens against this form of fraud through concrete measures focused on prevention, cooperation and awareness-raising. However, this fight cannot be conducted through banks alone. That is why the federal government is currently working on a national action plan to establish a cross-sector approach to online fraud.”

Jan Jambon, Deputy Prime Minister and Minister of Finance: “Online fraud is a form of organised crime that is constantly evolving. This action plan is an important step forward in the fight against online fraud. Banks play an essential role, but they cannot address this challenge alone. By strengthening prevention, information-sharing and cooperation between banks, public authorities and other stakeholders, we can make our response to fraud more effective.”