Mortgage lending remains steady in the second quarter of 2022

29 June 2022 - 10 min Reading time

In the second quarter of 2022, nearly 70,000 mortgage loan agreements were concluded, totaling more than 11.5 billion EUR (excluding refinancing).

This represents a decrease of nearly 5% in the number of granted loan agreements compared to the second quarter of the previous year. However, in terms of the loan amount, slightly more than 5% more credit was granted than at that time.

Excluding refinancing, the number of loan applications in the second quarter of 2022 decreased by almost 11% compared to the second quarter of 2021. There was also a decrease in the loan amount by approximately 7%.

These statistics come from mortgage credit data published today by the Professional Association of Credit (BVK).

The 49 members of the BVK collectively account for approximately 90% of the total number of newly granted mortgage loans (referred to as production). The total outstanding amount of mortgage credit held by the BVK members is approximately 266 billion EUR as of the end of June 2022.

Mortgage lending continues to reach new heights

After a very strong 2021 and an equally strong first quarter of 2022, the second quarter of 2022 saw a record amount of mortgage credit (in terms of amount) granted once again.

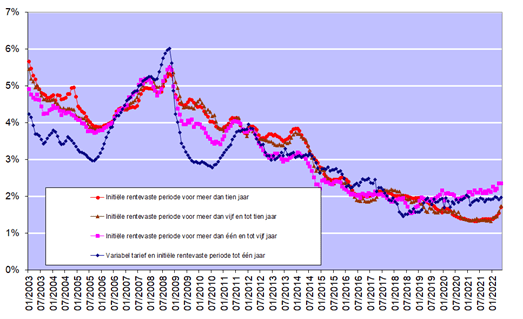

Interest rates for mortgage loans showed an upward trend in the past quarter but remained very attractive. According to figures published by the National Bank of Belgium, the rates in May ranged from an average of 1.70% (for loans with a fixed interest rate and an initial fixed interest period of more than 10 years) to an average of 2.35% (for loans with an initial fixed interest period of more than 1 year and up to 5 years).

"The second quarter of this year continued the momentum from the beginning of the year. Never before has such an amount of mortgage credit been granted in the second quarter, despite – or precisely because of – rising interest rates. We have been observing a reduced demand for credit for several months, which may be reflected in a decrease in lending in the coming months."

Here are the key findings (excluding refinancings) for the second quarter of 2022 compared to the second quarter of 2021:

- The number of credit applications (excluding those for refinancing) decreased by almost 11% in the second quarter of 2022 compared to the second quarter of 2021. The total amount of credit applications also decreased by approximately 7% compared to 2021. Therefore, slightly more than 99,000 credit applications were submitted for a total amount of 18 billion EUR.

- The granted mortgage loans decreased in number by almost 5% in the second quarter of 2022 compared to the same period last year. However, the corresponding total amount increased by more than 5% compared to 2021. In total, nearly 70,000 loans were granted for a total amount of more than 11.5 billion EUR (excluding refinancings)

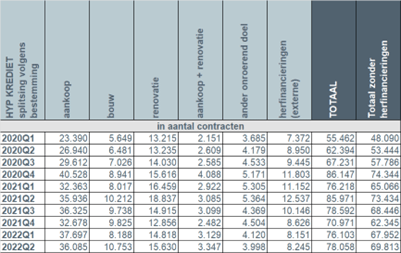

- The number of loans for other purposes (such as garage, land, etc.) experienced a significant decline in the second quarter compared to the same period in 2021 (-1,366 loans, or -25.5%). Similarly, the number of loans for home renovations decreased by 3,207 loans, which is a reduction of 17%. In contrast, the number of loans for home purchases remained relatively stable in the second quarter, increasing by approximately 0.4%, which is 149 loans more than in the second quarter of 2021. Additionally, the number of loans for home construction (+541 loans, or +5.3%) and loans for purchase with renovation (+262 loans, or +8.5%) experienced growth.

- The number of external refinancings decreased significantly by -4,292 loans, or -34.2%, in the second quarter of 2022. This decline is not surprising in the context of rising interest rates. However, more than 8,000 external refinancings were still granted in the second quarter of 2022, totaling more than 1.1 billion EUR.

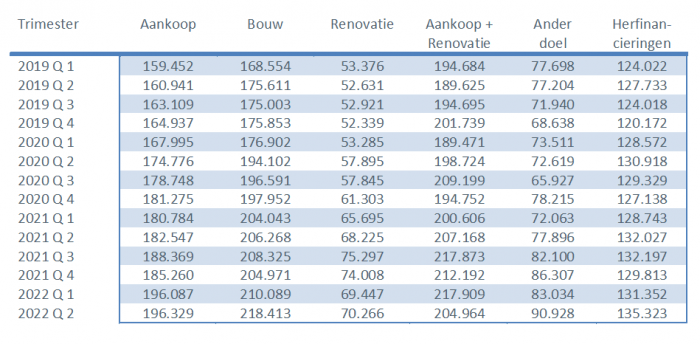

- The average amount borrowed for home purchases remained relatively stable at around 196,000 EUR in the second quarter of 2022. However, the average amount for construction loans increased to 218,000 EUR, marking an increase of nearly 50,000 EUR (or nearly 30%) since the beginning of 2019. The average amount for loans related to home purchase and renovation decreased slightly to approximately 205,000 EUR

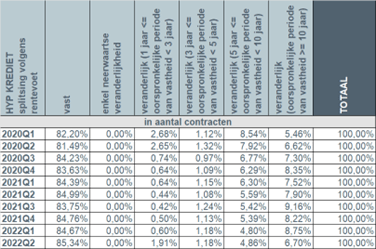

- In the second quarter of 2022, once again, more than 9 out of 10 borrowers (92%) opted for a fixed interest rate or a variable interest rate with an initial fixed interest period of at least 10 years. In less than 2% of cases, borrowers chose a loan with an annually variable interest rate.

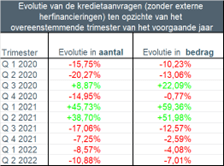

I. Number of loan applications

The number of loan applications (excluding those for refinancing) decreased by nearly 11% in the second quarter of 2022 compared to the same quarter of the previous year. The underlying loan amount also decreased by 7%.

The number of credit applications decreased for almost all purposes. Credit applications for the purchase of a home decreased by 4.3%, with a decrease of 2,610 applicatio. Credit applications for the purchase and renovation of a home decreased significantly by 26.8%, with a decrease of 1,901 applications. Credit applications for home renovations saw a strong decline of 21.4%, with 4,723 fewer applications. Credit applications for other purposes, such as garage, land, etc., experienced a notable decrease of 22.6%, resulting in 1,486 fewer applications. Credit applications for the construction of a home also decreased by 9.3%, with a reduction of 1,405 applications.The number of applications for external refinancing decreased substantially by 47.5%, which is not surprising given the current rising interest rate climate.

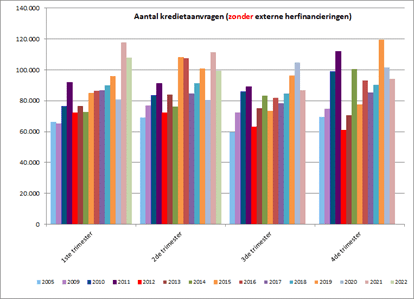

II. Number of granted credits in the second quarter

During the second quarter of 2022, the number of granted credits, excluding external refinancing, decreased by almost 5% compared to the second quarter of 2021. However, the corresponding total amount of credit granted increased by more than 5%.

Never before has so much mortgage credit (in terms of amount) been granted in a second quarter.

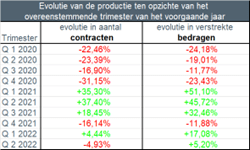

III. Mixed picture depending on the purpose of the credit

In the second quarter of 2022, nearly 70,000 new credits were granted for a total amount of just over 11.5 billion EUR, excluding external refinancing.

Overall, there was a decrease in the number of credits granted by almost 5% compared to the second quarter of 2021. However, it should be noted that there was not a decrease for all purposes compared to the previous year.

The number of credits for the purchase of a home increased slightly by 0.4% (149 more credits) compared to the second quarter of 2021. Credits for purchase with renovation increased by 8.5% (262 more credits), while construction credits were 5.3% higher (541 more credits). On the other hand, the number of credits for other purposes decreased by 25.5% (1,366 fewer credits), as did the number of credits for home renovations, which saw a decrease of 17% (3,207 fewer credits) compared to the second quarter of 2021.

Additionally, in the second quarter of 2022, the number of external refinancing credits decreased by 34.2%. Nevertheless, more than 8,000 external refinancing credits were granted, totaling more than 1.1 billion EUR.

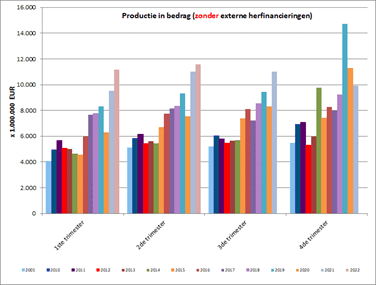

IV. Average amount of a credit for home construction increases by 50,000 EUR since early 2019

In the second quarter, the number of credits granted decreased, but the total amount of credit granted increased. This indicates that, in general, the average amount of granted credits has risen, with the exception of credits intended for purchase with renovation.

The average amount of a credit for home construction experienced a very significant increase during the second quarter of 2022, reaching 218,000 EUR. This represents an increase of approximately 50,000 EUR (or 29.6%) since early 2019.

The average amount of a credit for the purchase of a home stabilized at around 196,000 EUR in the second quarter of 2022. However, this still represents an increase of approximately 37,000 EUR (or 23%) over just over three years.

The average amount of a credit for the purchase of a home with renovation decreased to approximately 205,000 EUR.

V. Still more than 9 out of 10 borrowers opt for a fixed interest rate

In the second quarter of 2022, more than 9 out of 10 borrowers (92%) once again chose either a fixed interest rate or a variable interest rate with an initial fixed rate period of at least 10 years. Approximately 6% of borrowers opted for a variable interest rate with an initial fixed rate period of 3 to 10 years, while slightly less than 2% of borrowers chose an annually variable interest rate.

Taking into account the rising but still low interest rates (see chart below), Belgian consumers overwhelmingly continue to choose certainty. The number of individuals opting for a variable interest rate remains low, especially regarding annually variable interest rates. However, even in the case of a variable interest rate, consumers are strongly protected by legislation. After adjustment to the evolution of the applicable reference indexes, the variable interest rate can never exceed twice the initial interest rate.

Responsible mortgage lending remains the guiding principle.

The credit sector is and remains aware that mortgage lending must be conducted with great care, and responsible lending must remain the absolute priority. In this regard, the sector aligns with the regulator: credit providers must exercise caution to prevent individual borrowers from taking on overly substantial loans and, at the same time, safeguard financial stability in the long run.