High demand for mortgage loans in the third quarter

29 October 2020 - 10 min Reading time

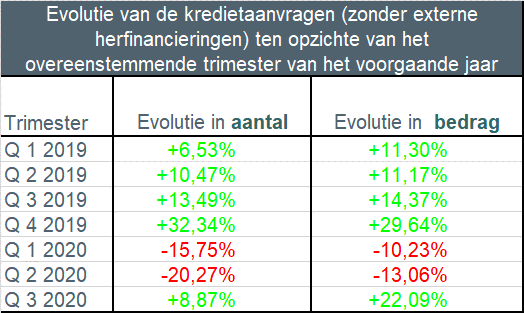

Excluding refinancing, the number of loan applications in the third quarter of 2020 increased by just under 9% compared to the third quarter of 2019. There was also an increase of approximately 22% in terms of the loan amount.

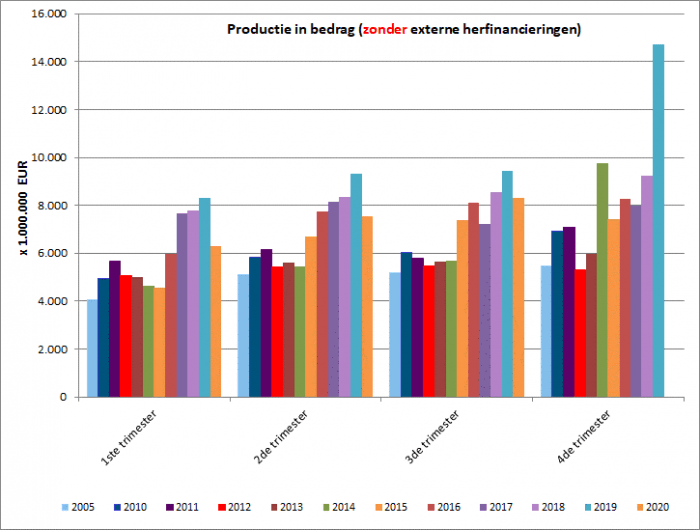

In the third quarter of 2020, nearly 58,000 mortgage loan agreements were concluded for a total amount of approximately 8.3 billion EUR (excluding refinancing).

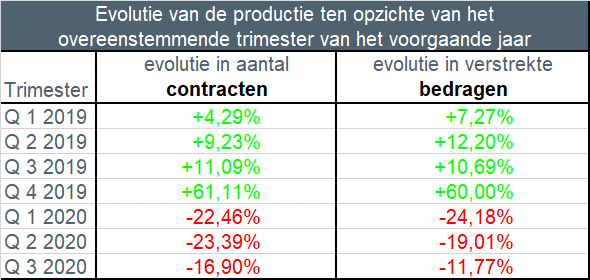

However, this still represents a decrease in the number of granted loan agreements by about 17% compared to the third quarter of the previous year. In terms of the amount lent, nearly 12% less credit was granted than before.

The increasing number of loan applications in this quarter has not yet translated into an increase in the number of loans granted. Since there can be a three to four-month period between the signing of the loan and the execution of the loan agreement, such as in the case of a home purchase, this is likely to become visible only next quarter. In September, however, more mortgage loans were granted than in the same month of the previous year for the first time this year.

This information is based on mortgage credit statistics published today by the the Professional Association of Credit (BVK).

De 54 leden van de BVK nemen samen ongeveer 90% van het totaal aantal nieuw verstrekte hypothecaire kredieten (de zogeheten productie) voor hun rekening. Het totale uitstaande bedrag aan hypothecair krediet van de BVK-leden bedraagt eind september 2020 ongeveer 241 miljard EUR.

Gradual recovery in mortgage loan lending

Due to the COVID-19 crisis and the associated government measures such as the ban on non-essential travel, closure of non-essential sectors, etc., mortgage lending experienced a sharp decline in the second quarter. In the third quarter, the real estate market and the demand for mortgage loans started to recover, but this increased demand has not yet been reflected in the loan approval figures.

Nevertheless, the situation appears to be slowly improving. In the month of September, more mortgage loans were granted than in the same month of the previous year for the first time this year.

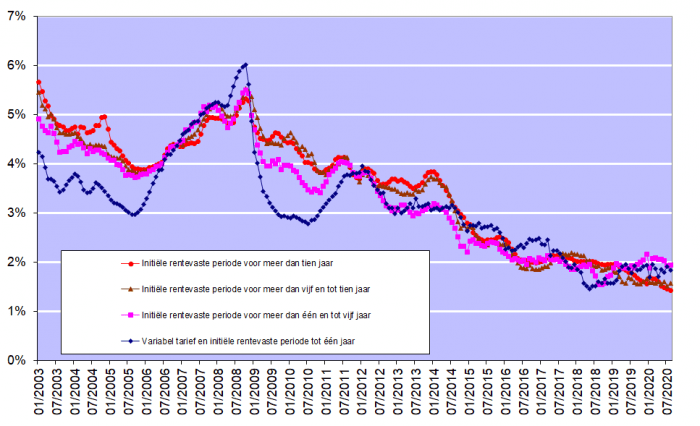

In the past quarter, borrowers were able to take advantage of very low interest rates for mortgage loans. According to figures published by the National Bank of Belgium, interest rates in August ranged from 1.42% (for loans with a variable interest rate and an initial fixed interest period of more than 10 years) to 1.94% (for loans with an initial fixed interest period of more than 1 year and less than 5 years).

Below you will find the key findings for the third quarter of 2020 compared to the third quarter of 2019 (these figures exclude refinancing).

- The number of credit applications (excluding those for refinancing) increased by just under 9% in the third quarter of 2020 compared to the third quarter of 2019. The total amount of credit applications also increased by about 22%. As a result, nearly 105,000 credit applications were submitted for a total amount of more than 17 billion EUR.

- The granted mortgage loans decreased in number by almost 17% in the third quarter of 2020 compared to the same quarter last year. The corresponding amount decreased by nearly 12%. In total, almost 58,000 loans were granted for a total amount of 8.3 billion EUR (excluding refinancing).

- During the month of September, for the first time this year, there was an increase in the amount of credit granted compared to the same month of the previous year. It was about 1%, but it may potentially mark the starting point for further recovery.

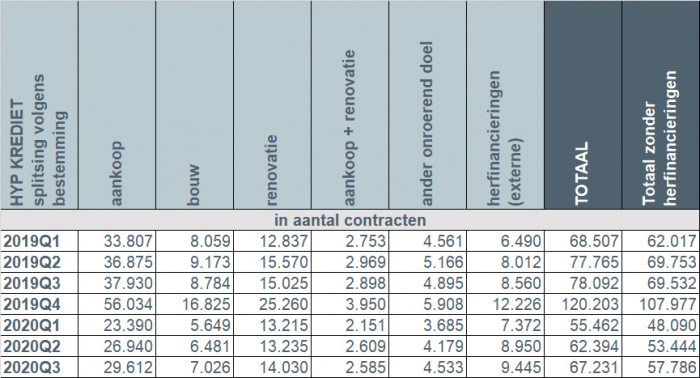

- The number of loans for the purchase of a home experienced the strongest percentage decrease in the third quarter, namely -21.9%, or 8,319 fewer loans than in the third quarter of 2019. The number of construction loans (-1,758) decreased by 20%, while the number of loans for purchase with renovation (-315) decreased by 10.9%. The number of loans for the renovation of a home (-995, or -6.6%), as well as the number of loans for other purposes (e.g., garages, land) (-362, or -7.4%), also decreased compared to the third quarter of 2019.

- The number of external refinancings (+885) continued to increase in the third quarter of 2020, by 10.3% compared to the third quarter of 2019. Specifically, approximately 9,500 external refinancings were granted for more than 1.2 billion EUR in the third quarter of 2020.

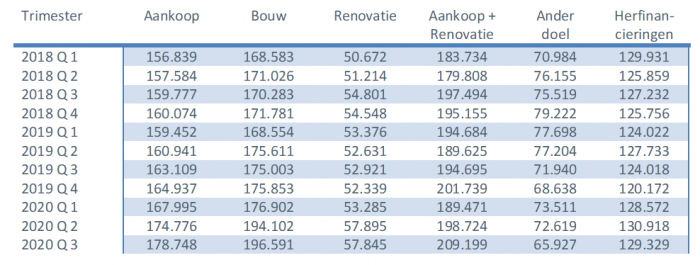

- The average amount of loans for home purchase and renovation continues to rise significantly and has surpassed 209,000 EUR for the first time, breaking the 200,000 EUR threshold. The average borrowed amount for the purchase of a home also increased to nearly 179,000 EUR in the third quarter of 2020, while the average amount for construction loans reached approximately 196,500 EUR.

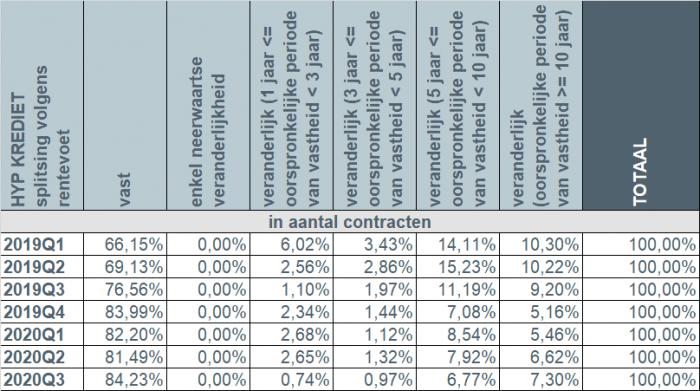

- In the third quarter of 2020, more than 9 out of 10 borrowers chose a fixed interest rate or a variable interest rate with an initial fixed interest period of at least 10 years. In less than 1% of cases, a loan with an annually adjustable interest rate was chosen.

Number of Loan Applications

The number of loan applications, excluding those related to external refinancing, increased by nearly 9% during the third quarter of 2020 compared to the same quarter of the previous year. The underlying loan amount also increased by more than 22%.

Loan applications increased for all purposes. Loan applications for home purchases (+5,151) increased by 9.3%, those for home purchase and renovation (+1,432) by almost 28%. The number of loan applications for construction of a home (+333, or +3%) and for home renovation (+728, or +4%) also increased, as did the number of loan applications for other purposes (e.g., garages, land) (+878, or +14%). Loan applications for external refinancings also increased by 25.4%.

Number of loans granted in the third quarter

In the third quarter of 2020, the number of loans granted, excluding external refinancing, decreased by almost 17% compared to the same quarter of the previous year. The corresponding amount decreased by nearly 12%.

During the month of September, more mortgage loans were granted than in the same month of the previous year for the first time this year, albeit at a limited increase of 1.2%. Nonetheless, this may mark the beginning of further growth.

The total amount of loans granted in the third quarter is lower than in the third quarter of the peak year 2019 but still approaches the very high level of the year 2018.

Decrease in the number of loans for all purposes

In the third quarter of 2020, slightly fewer than 58,000 new loans were granted for a total amount of approximately 8.3 billion EUR, excluding external refinancing.

Compared to the third quarter of the previous year, there was a decline observed for all purposes.

The number of loans for home purchases (-8,319) in the third quarter of 2020 was almost 22% lower than in the third quarter of 2019. The number of loans for purchase with renovation (-315) decreased by 10.9%, while the number of construction loans (-1,758) was down by 20%. The number of loans for other purposes (-362) decreased by 7.4%. Additionally, the number of loans for home renovations decreased by 6.6%, which is 995 fewer loans than in the third quarter of 2019.

Furthermore, in the third quarter of 2020, the number of external refinancings (+885) continued to be the only one showing an increase, by 10.3% compared to the third quarter of 2019. Approximately 9,500 external refinancings were granted for a total amount of just over 1.2 billion EUR.

Average loan amount for home purchase with renovation exceeds 200,000 EUR

The average loan amount for home purchase with renovation experienced another significant increase to 209,000 EUR in the third quarter. This is an increase of more than 25,000 EUR (or 14%) since the beginning of 2018.

The average loan amount for home purchase also continued to rise in the third quarter of 2020, reaching nearly 179,000 EUR. This represents an increase of 22,000 EUR compared to the beginning of 2018.

The average loan amount for construction loans further increased to over 196,000 EUR in the third quarter of 2020. This marks an increase of more than 28,000 EUR since the beginning of 2018.

More than 9 out of 10 borrowers opt for a fixed interest rate

In the third quarter of 2020, more than 9 out of 10 borrowers (91.5%) chose either a fixed interest rate or a variable interest rate with an initial fixed interest period of at least 10 years. Just under 8% of borrowers opted for a variable interest rate with an initial fixed interest period between 3 and 10 years. The number of borrowers opting for an annually variable interest rate fell to just 0.7%.

Considering the still very low interest rates (see chart below), Belgian consumers continue to overwhelmingly choose certainty. The number of individuals opting for a variable interest rate is decreasing, especially concerning the annually variable interest rate. However, even in the case of a variable interest rate, consumers are highly protected by legislation. After adjusting to changes in applicable reference indexes, the variable interest rate can never exceed double the initial interest rate.

Responsible mortgage lending remains the primary focus

The credit sector is and remains aware that mortgage lending must be done with great care, and responsible lending should remain the absolute priority. In this regard, the sector aligns with the regulator: credit providers must exercise caution to maximize the avoidance of individual borrowers taking out excessively large loans while safeguarding financial stability in the long term.