The digital euro: simplicity as the guiding principle, phased implementation as a prerequisite

23 June 2026 - 6 min Reading time

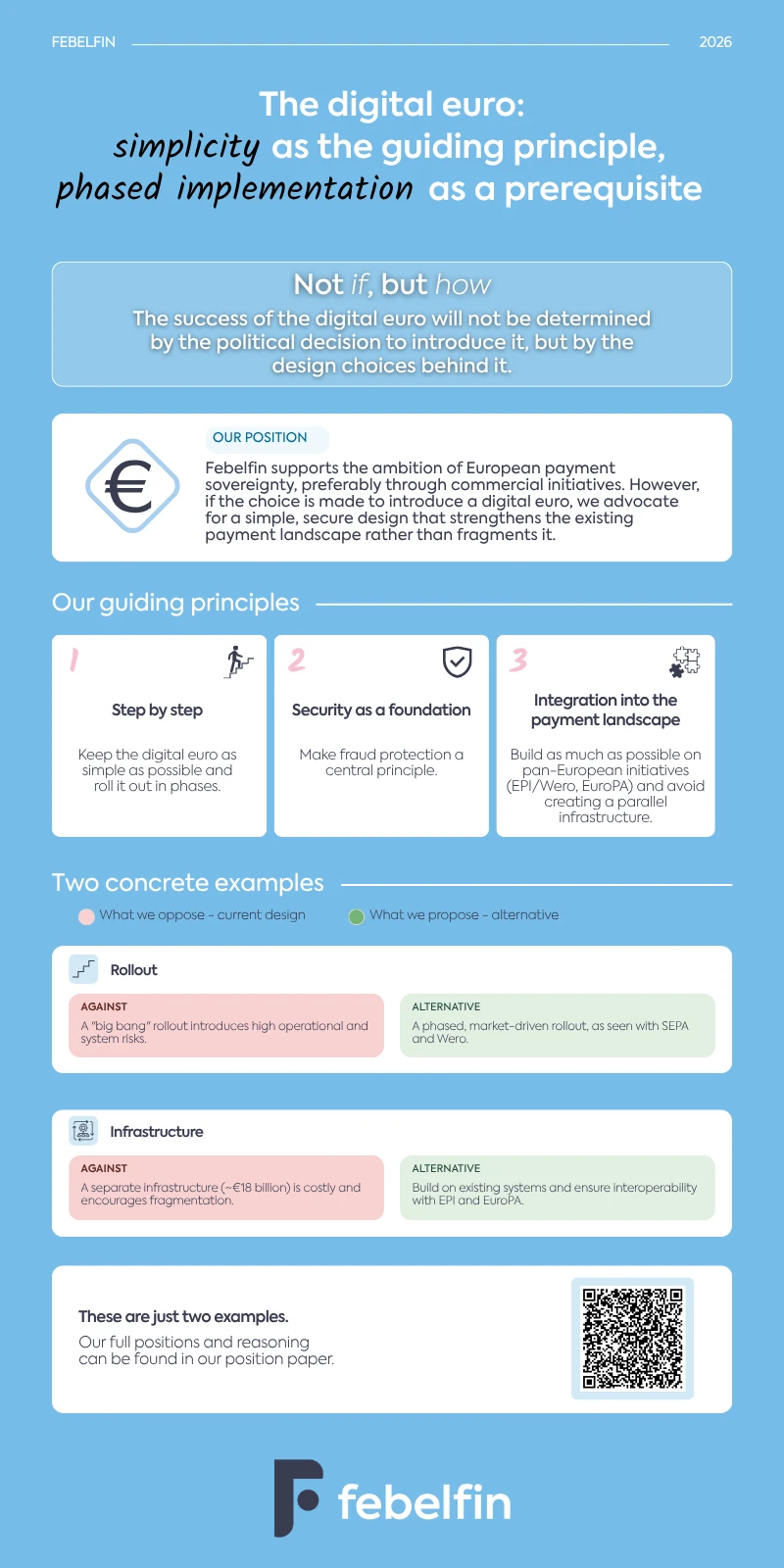

On 23 June, the European Parliament’s position on the digital euro was approved. This approval marks the beginning of the final phase of the political negotiations on the digital euro. Febelfin regrets that the European legislators have chosen not to further strengthen existing, high-performing and European private payment systems in support of European autonomy, but to introduce a public payment system instead. We nevertheless accept this political decision.

Despite the sector’s objections, we would like to share a number of recommendations to make its implementation feasible, drawing on our extensive experience in developing and maintaining some of the world’s safest payment systems. The design of the digital euro is essential to ensure that its implementation is workable. An overly complex model risks generating high costs and increasing operational risks. It is therefore of great importance that both the further development and the final legislative text are guided by a number of clear principles. To that end, Febelfin sets out three clear recommendations:

1. Phased implementation

Febelfin advocates a phased implementation of the digital euro. The current proposals immediately provide for a very broad and complex system covering all types of payments, which entails significant operational and system risks. Febelfin therefore proposes starting with a concrete and limited scope: one account per user, one specific use case – namely payments between individuals – and limited offline functionality, from which the system can then be further developed. Practice shows that successful payment innovations are always rolled out in stages.

In addition, Febelfin advocates applying a low holding limit so that the digital euro remains purely a means of payment and does not become a savings or investment instrument, thus avoiding pressure on the financing of the real economy. We must not forget that savings deposits constitute an important basis for banks to be able to grant credit to households, businesses and government.

EPI (European Payments Initiative) is een pan-Europees initiatief van banken en betaalinstellingen dat tot doel heeft een uniforme Europese betaaloplossing te ontwikkelen, met onder meer de digitale wallet Wero. EuroPA (European Payments Alliance) is een samenwerking tussen bestaande mobiele betaaloplossingen (zoals Bizum, Bancomat en MB Way) die interoperabiliteit tussen nationale betaalsystemen mogelijk maakt en zo grensoverschrijdende betalingen binnen Europa vereenvoudigt.

2. Security is central

Febelfin emphasises that fraud prevention and consumer protection must be central from the outset. In this respect, the automatic funding mechanism (“waterfall system”) calls for particular vigilance. Within this model, payments are automatically funded from linked bank accounts when the digital euro balance is insufficient, without the user’s explicit confirmation. It is however essential that funding the digital euro account always takes place with the customer’s explicit consent, in order to limit the risk of fraud. For Belgian banks, the fight against fraud is a top priority, and the security of online payments must not be compromised by the digital euro.

3. Integration into the existing European payments landscape

Both in the legislative text and in the further technical development of the digital euro, maximum use should be made of existing European payment infrastructures and initiatives such as EPI (including Wero) and EuroPA.

According to Febelfin, a completely new infrastructure for the digital euro would generate high costs and additional fragmentation, whereas integration with existing solutions can deliver scale, efficiency and ease of use more quickly.

It is therefore advisable to reuse as much as possible of what is already working today and is secure and reliable. In this way, the digital euro can strengthen and further develop existing European payment solutions, rather than further fragmenting the European payments landscape.

EPI (European Payments Initiative) is een pan-Europees initiatief van banken en betaalinstellingen dat tot doel heeft een uniforme Europese betaaloplossing te ontwikkelen, met onder meer de digitale wallet Wero. EuroPA (European Payments Alliance) is een samenwerking tussen bestaande mobiele betaaloplossingen (zoals Bizum, Bancomat en MB Way) die interoperabiliteit tussen nationale betaalsystemen mogelijk maakt en zo grensoverschrijdende betalingen binnen Europa vereenvoudigt.

In conclusion

Febelfin emphasises that the success of the digital euro will depend on realistic, secure and efficient implementation. A simple design and phased implementation are essential in order to limit operational risks and leave sufficient room for evaluation and adjustment. Fraud prevention must also take priority. Finally, Febelfin advocates making the greatest possible use of existing European payment infrastructures and initiatives, so as to avoid unnecessary costs and further fragmentation of the European payments landscape. If the digital euro is introduced, we must ensure that it can develop into a workable complement to the existing payments system, without jeopardising the stability, security and efficiency of the current financial ecosystem.

The big picture in one look