Mortgage credit peaks in the first quarter

10 min Reading time

Excluding refinancings, the number of loan applications increased by 46% in the first quarter of 2021 compared to the first quarter of 2020. There was also an increase in amount by approximately 59.5%.

In the first quarter of 2021, 65,000 mortgage loan agreements were concluded for a total amount of approximately EUR 9.5 billion (excluding refinancings).

This also means an increase in the number of credit agreements granted by approximately 35% compared to the first quarter of last year. In terms of amount, approximately 51% more credit was provided than at the time.

In all this, it should not be forgotten that the first quarter of 2020 was a rather weak quarter after the abolition of the housing bonus in Flanders at the end of 2019 and the fact that many borrowers therefore canceled their financing projects (purchase, construction and renovation) at the end of 2019. had completed early, but also due to the start of the corona crisis in March.

But a comparison with the first quarter of 2019 also shows that strong figures were achieved in the past quarter.

These conclusions can be found in the statistics on mortgage credit that the Professional Association of Credit (BVK) published today.

The 54 members of the BVK together account for approximately 90% of the total number of newly granted mortgage loans (so-called production). The total outstanding amount of mortgage credit of BVK members amounts to approximately EUR 246 billion at the end of March 2021.

Mortgage lending has fully recovered

The recovery of the real estate market and demand for mortgage credit continued in the first quarter of 2021, after the already strong last quarter of 2020.

On the one hand, this concerns catching up after the special "corona year" 2020 and the urge among consumers for a better home situation due to increased working from home and restrictions on holiday options.

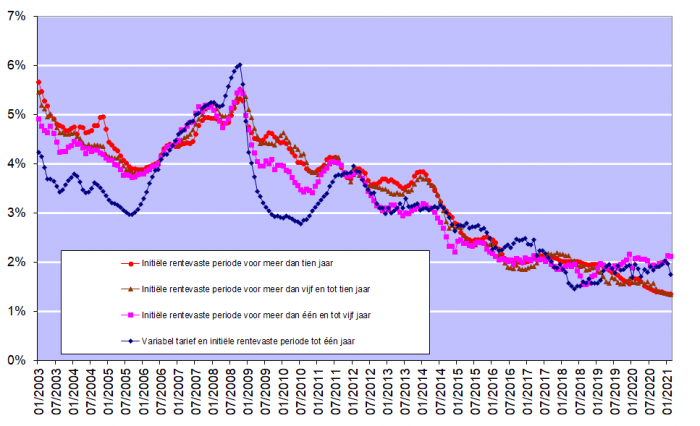

But on the other hand, interest rates for mortgage loans also remained very attractive in the past quarter. According to figures published by the National Bank of Belgium, in February they amounted to between 1.34% (for loans with a variable interest rate and an initial interest rate fixation period of more than 5 years and up to 10 years) and 2.12% (for loans with an initial fixed interest period of more than 1 year and up to 5 years).

Below you will find the most important findings for the first quarter of 2021 compared to the first quarter of 2020:

Bij deze cijfers zijn de herfinancieringen buiten beschouwing gelaten.

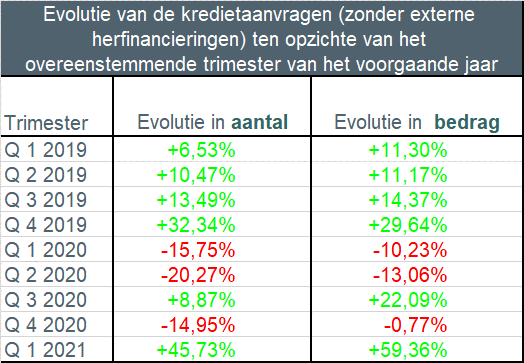

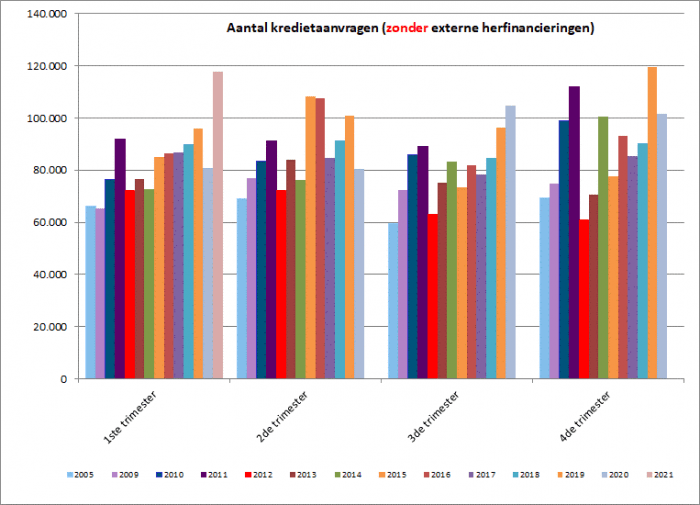

- The number of credit applications (excl. those for refinancing) increased by just under 46% in the first quarter of 2021 compared to the first quarter of 2020. But there was also an increase of almost 23 compared to the first quarter of 2019. %. The amount of credit applications also increased by approximately 60% compared to 2020. Nearly 118,000 credit applications were therefore submitted for a total amount of exactly EUR 20 billion. An absolute record for a first trimester.

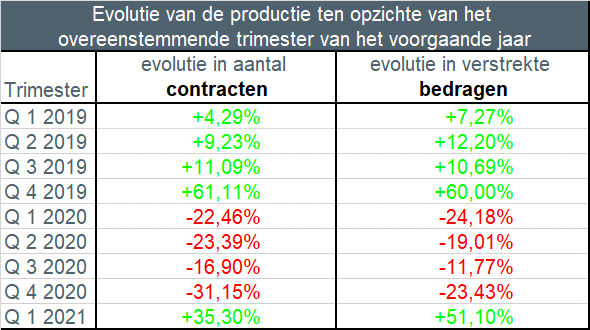

- Mortgage loans granted increased by more than 35% in the first quarter of 2021 compared to the first quarter of last year. But there is also an increase of almost 5% compared to the first quarter of 2019. The corresponding amount increased by just over 51% compared to 2020. A total of just over 65,000 loans were granted for a total amount of EUR 9.5 billion (excl. refinancings).

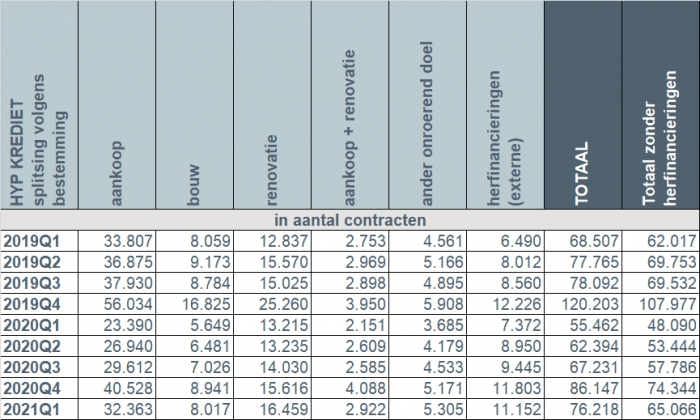

- The number of loans for the construction of a home saw the strongest increase in percentage terms in the first quarter, i.e. +42% or 2,368 more loans than in the first quarter of 2020, together with the number of loans for other purposes (+1,620, or + 44%) (garage, building land,...). The number of loans for the purchase of a home (+8,973) increased by 38.4%, while the number of loans for purchase with renovation (+771) increased by almost 36%. The number of loans for the renovation of a home (+3,244, or +24.5%) also increased compared to the first quarter of 2020.

- The number of external refinancings (+3,780) also continued to increase in the first quarter of 2021 by 51.3% compared to the first quarter of 2020. More than 11,000 external refinancings were provided in the first quarter of 2021 for more than 1. EUR 4 billion.

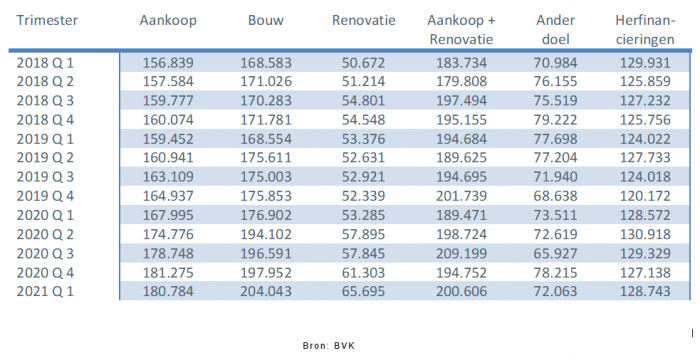

- The average amount for a construction loan broke the EUR 200,000 barrier for the first time in the first quarter of 2021, at EUR 204,000. That is an increase of EUR 36,000 (or 21%) in two years. The average amount of credits for purchase + renovation also fluctuated around EUR 200,000. The average amount borrowed for the purchase of a home remained approximately stable at around EUR 181,000 in the first quarter of 2021.

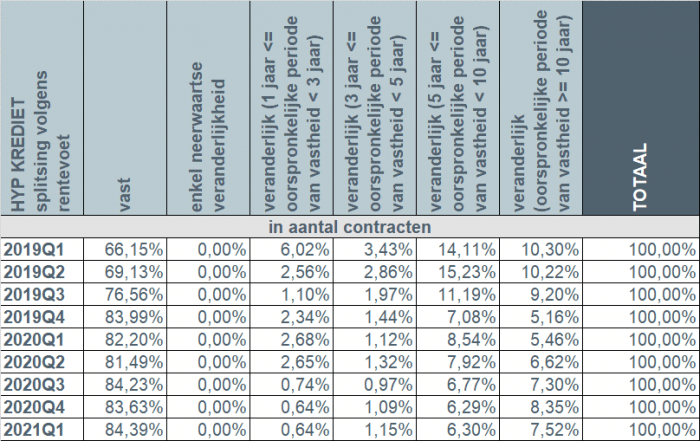

- In the first quarter of 2021, more than 9 out of 10 borrowers again opted for a fixed interest rate or a variable interest rate with an initial interest rate fixation period of at least 10 years. In only 0.6% of cases a credit with an annually variable interest rate was opted for.

I. Number of credit applications

The number of credit applications, excluding those relating to external refinancing, increased by almost 46% during the first quarter of 2021 compared to the same quarter of last year. The underlying amount of credit applications also increased by almost 60%.

The number of credit applications increased for all purposes. Loan applications for the purchase of a home (+15,788) increased by 35.5%, those for the purchase + renovation of a home (+3,212) by almost 69%. The number of credit applications for the construction of a home (+6,411, or +66.7%) and for the renovation of a home (+9,209, or +55.3%) also saw a strong increase, as did the number of credit applications for other purposes (+2,359, or +43.2%). The number of applications for external refinancing also increased again by 49%.

Garage, bouwgrond, …

Never before have so many credit applications been submitted.

II. Number of loans granted in the first quarter

In the first quarter of 2021, the number of loans granted, excluding external refinancings, increased by more than 35% compared to the first quarter of 2020. The corresponding amount increased by more than 51%.

Never before has so much mortgage credit been granted in a first quarter.

III. Increase in the number of credits for all purposes

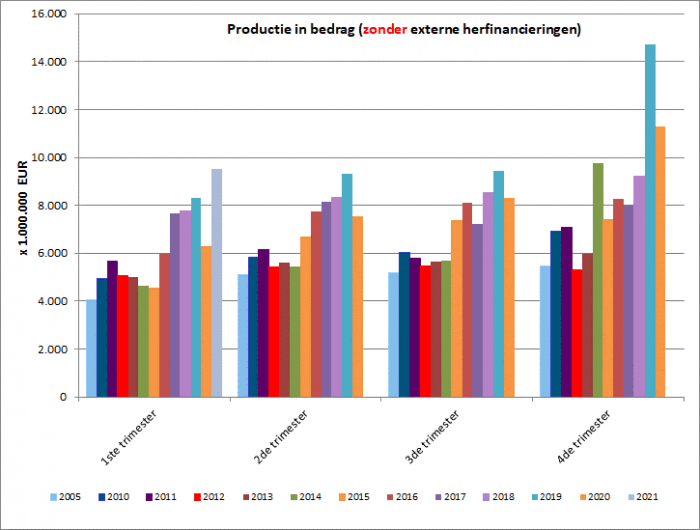

Just over 65,000 new loans were granted in the first quarter of 2021 for a total amount of approximately EUR 9.5 billion – excluding external refinancings.

Compared to the first quarter of last year, an increase was observed for all purposes.

The number of loans for the purchase of a home (+8,973) was more than 38% higher in the first quarter of 2021 than in the first quarter of 2020. The number of loans for purchase with renovation (+771) increased by almost 36 %, while the number of construction loans (+2,368) was 42% higher. The number of loans for other purposes (+1,620) increased by 44%. The number of loans for the renovation of a home also increased, namely +24.5% or 3,244 loans more than in the first quarter of 2020.

In addition, the number of external refinancings continued to increase by more than 51% in the first quarter of 2021. In particular, just over 11,000 external refinancings were provided for a total amount of just over EUR 1.4 billion.

IV. Average amount of a loan for the construction of a home breaks the barrier of EUR 200,000

The average amount of a loan for the construction of a home increased further in the first quarter of 2021, breaking the EUR 200,000 barrier. With an average amount of EUR 204,000, this represents an increase of more than EUR 36,000 (or 21%) since the beginning of 2019.

The average amount of a loan for the purchase of a home + renovation also exceeded the EUR 200,000 limit again in the first quarter, at EUR 200,606. Nevertheless, this is “only” an increase of approximately EUR 6,000 (or 3%) since the beginning of 2019.

The average amount of a loan for the purchase of a home continued to fluctuate around EUR 181,000 in the first quarter of 2021. This is also an increase of EUR 21,000 (or 13.4%) compared to the beginning of 2019.

V. More than 9 out of 10 borrowers opt for a fixed interest rate

In the first quarter of 2021, more than 9 in 10 borrowers (92%) again opted for a fixed interest rate or a variable interest rate with an initial interest rate fixation period of at least 10 years. Just over 7% of borrowers opted for a variable interest rate with an initial interest rate fixation period between 3 and 10 years. The number of borrowers who opted for an annually variable interest rate is barely 0.6%.

In the first quarter of 2021, more than 9 in 10 borrowers (92%) again opted for a fixed interest rate or a variable interest rate with an initial interest rate fixation period of at least 10 years. Just over 7% of borrowers opted for a variable interest rate with an initial interest rate fixation period between 3 and 10 years. The number of borrowers who opted for an annually variable interest rate is barely 0.6%.

Responsible mortgage lending remains the starting point

The credit sector is and remains aware that mortgage lending must be done with great care and that responsible lending must remain the absolute starting point. On this point, the sector is on the same page as the regulator: lenders must exercise the necessary caution to, on the one hand, prevent individual borrowers from taking out loans that are too large and, on the other hand, to safeguard financial stability in the long term.